")

piola666

Shell plc (NYSE: SHEL) is currently rowing back on its decarbonization initiatives seen over the past half decade as management focuses the company’s resources on maximizing shareholder value. This transition is centered on liquids and gases production and a strong focus on its integrated gas business by expanding its LNG trading footprint. Despite this turnaround, I believe management will remain prudent in equipping the company’s operations to meet demand as the energy transition takes greater hold over the rest of the decade with respect to renewable fuels and biofuels. Given Shell’s increased focus on maximizing and optimizing operations, I recommend SHEL shares with a Buy rating and a price target of $78.56/share at 4.06x eFY25 EV/aEBITDA.

Shell operations

FinChat

Shell is currently undergoing major changes in the company’s attitude towards energy and decarbonization. It has been less than three years since Shell completed the sale of its Permian Basin assets to ConocoPhillips. (POLICEMAN) in December 2021, at a time when the Dutch oil company was steering the ship towards more renewable energy. Fast forward to their last capital markets dayThe company expects to increase production by 500 Mboe/d by 2025. Whether all this was part of the plan is questionable, but one thing is certain: management is shelving less profitable biofuel projects in favor of hydrocarbons.

But that doesn’t mean the company is ignoring biofuels altogether. Projects will likely be postponed until the end of the decade, when demand is expected to pick up again. Although there is great interest in biofuels, the adoption of these sustainable fuels is not progressing as quickly as expected, creating a mismatch between capital expenditure and demand. With higher raw material costs and falling product prices, today’s economic conditions simply do not suit Shell’s business. As a result, management has decided to shut down the Rotterdam plant, which was supposed to be one of the largest production facilities for sustainable aviation fuel and renewable diesel.

The regional governments are also not providing any help in this matter. According to an article by ReutersSweden has cut its biofuel mandates. Finland and Germany have also cut their biofuel mandates, making the practice of fuel blending less attractive from an economic perspective. Management has largely not abandoned its long-term strategy of biofuel production. However, management indicated in the second quarter 2024 earnings call that government mandates will likely be needed to bring more demand into this market.

Ironically, just as Shell is focusing more on hydrocarbons, the British government has launched a multi-billion dollar initiative to anchor the country even more firmly in renewable resources. According to the Wall Street JournalGreat British Energy, a government-backed investment initiative funded by taxes on oil and gas production, has around $11 billion to invest in renewable projects in the region, boosting the country’s onshore wind and solar capacity over the next 5-6 years. This initiative does not seem to have gone down well with the oil giant, as it could undermine energy stability.

However you play, stability is key. Further changes to the goalposts only undermine the element of stability we advocate.

Wael Sawan, CEO, Shell

Looking at oil and gas production, management’s focus on maximising shareholder value has become more evident in recent quarters as the company shifts its emphasis back to hydrocarbons. This includes investments in oil and gas developments and LNG terminals. On the integrated gas side of the business, Shell is actively increasing its presence in the LNG trading sector by building or acquiring liquefaction facilities. This includes Shell’s recent acquisition of Pavilion Energy, which will bring in 6.5 MTPA of contracted supply. In addition, Shell is working with ADNOC Ruwais LNG on a project in Abu Dhabi and has taken on FID for the Manatee Backfill project in Trinidad and Tobago.

Shell Finances

Corporate reports

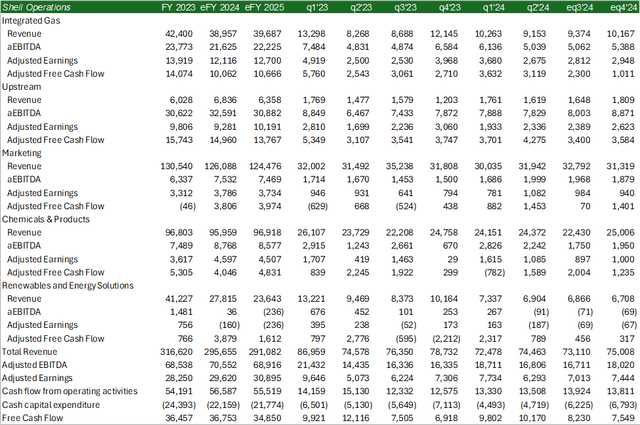

In setting out the financials for Shell, management set a relatively flat production rate for the future as the company manages its liquidity position. Total production from all segments is expected to increase by an additional 250 Mboe/d by 2025 as the company brings additional gas fields and offshore rigs online in the Gulf of Mexico and Brazil. These include Vito and Rydberg in the Gulf of Mexico, Mero-2 in Brazil, Block 10 in Oman, and Timi and Jerun in Malaysia. Shell has other projects underway, including Mero-3 in Brazil and Penguins in the North Sea. The company has taken on FID for Atapu-2 in Brazil and Sparta in the Gulf of Mexico. Management expects these investments to keep LNG production in the 1.4 MMbbl/d range through the end of the decade.

In renewables and energy solutions, management is focused on upgrading its portfolio to support the future energy transition. This includes exiting the Home Energy business in Europe in 2023, and this segment is likely to continue to shrink by the end of the decade. Despite the slowdown in renewables, Shell announced the FID for Polaris in Canada, its carbon capture and storage project that is expected to capture 650,000 tonnes of CO2 annually. Shell also announced the FID with the Atlas Carbon Storage Hub in partnership with ATCO EnPower as part of the Polaris project. These projects are expected to come online towards the end of 2028. In chemicals, Shell withdrew from the Energy and Chemicals Park in Singapore and its ownership rights to the PCK refinery in Germany.

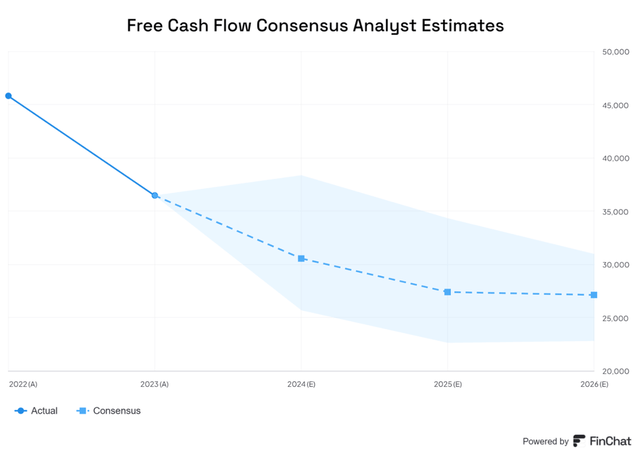

Converting this to cash flow, I forecast Shell to generate free cash flow of $36.75 billion in eFY24 and $35.37 billion in eFY25. The decline in eFY25 is the result of the decline curve that puts Brent futures in the mid to low $70s per barrel in 2025, coupled with stronger pricing in natural gas futures.

Valuation & Shareholder Value

Corporate reports

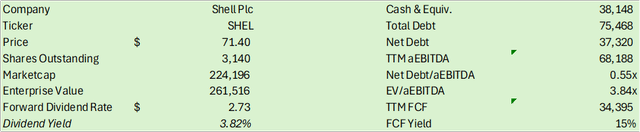

SHEL shares trade at a premium to European peers and remain well below domestic IOCs. I am confident the company is taking the right steps to create additional value for shareholders and move closer to domestic peers. For example, management announced a $3.5 billion share buyback program for eq3’24, which should be completed by the end of the quarter. Shell also has a strong dividend yield of 3.82% compared to Exxon Mobil (XOM) and Chevron (CVX); however, this is below the overall cohort average of 4.4%.

I’m looking for Alpha

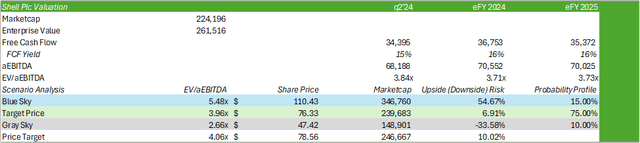

Based on my cash flow generation forecast, I believe SHEL shares are slightly undervalued at their current premium of 3.84x trailing EV/aEBITDA. I believe the company has some room to increase its trading multiple if management continues its robust share buyback program. I rate SHEL shares a Buy with a price target of $78.56/share at 4.06x eFY25 EV/aEBITDA.

Corporate reports