")

Marvin Samuel Tolentino Pineda/iStock via Getty Images

introduction

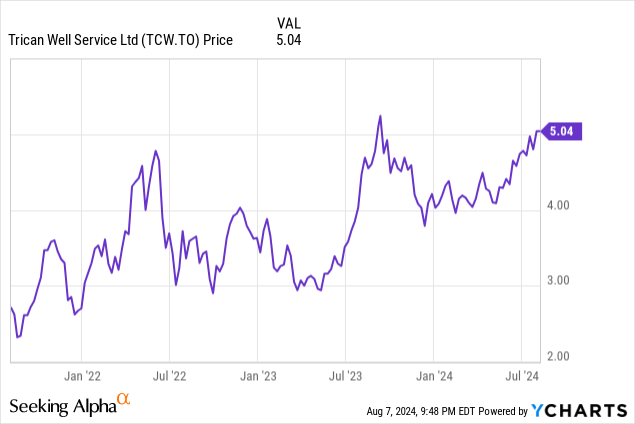

About 15 months ago I wrote an article about Trican Well Service (OTCPK:TOLWF, TSX:TCW:CA) because I liked the strong balance sheet of this oil and gas services provider provider. And despite the recent turmoil in the financial markets, the share price is still about 65% higher than at the time of writing in May 2023. The strong share price is supported by good financial results, and although the second quarter is traditionally quite weak for O&G service companies, Trican Well Service has performed surprisingly well.

A relatively strong second quarter despite the spring break

As a service provider to the oil and gas industry, Trican Well has to deal with seasonality. The second quarter is usually the weakest, while the other three quarters are much stronger. This is Why it would not be a good idea to extrapolate second quarter or first half year results to estimate full year expectations, as the second half is likely to be significantly better than the first.

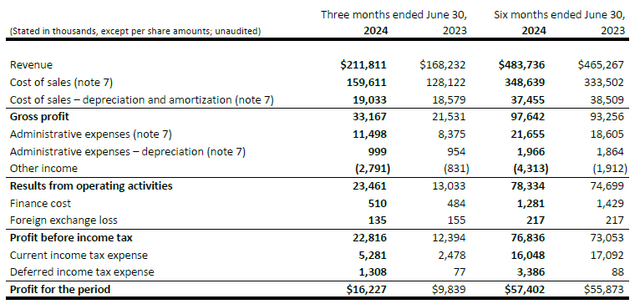

Still, Trican’s second quarter results were a pleasant surprise. The company was able to increase revenue by about 25%, and efficiency gains helped gross profit increase by more than 50% to C$33.2 million. And although administrative expenses increased quite a bit (due to the settlement of stock awards), operating income increased by over C$10 million to C$23.5 million.

Investor Relations with Trican Well

In addition, net financial costs and foreign exchange expenses remained low, resulting in pre-tax profit of CAD$22.8 million and net profit of CAD$16.2 million. This represents earnings per share of CAD$0.08 and an increase of 75% compared to the second quarter 2023 results, where the company reported earnings per share of CAD$0.045. This increase in profit was mainly due to the 65% increase in net profit, while the company also reduced its average share count, and therefore the increase in earnings per share is stronger than the increase in net profit expressed in Canadian dollars.

And once again, Q2 is the weakest quarter for Trican Well Service. Looking at the first half results, we see gross profit of CAD 97.6 million and operating profit of CAD 78.3 million, an increase of about 5% over the first half of last year. The impact on reported net income was not as impressive (net income only increased by 3%), but thanks to the sharp reduction in the average share count, earnings per share increased from CAD 0.251 to CAD 0.279, an increase of about 11%.

One of the main reasons I started following Trican Well Service was its excellent ability to convert revenue and EBITDA into free cash flow.

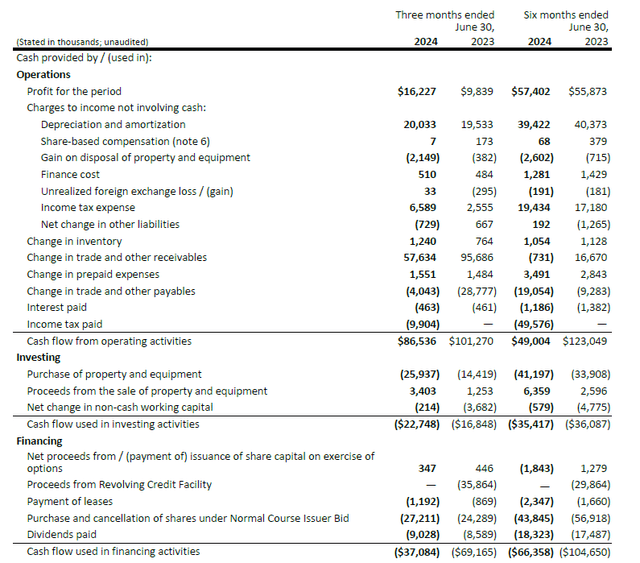

Looking at the second quarter results, we see operating cash flow of $86.5 million, however this was boosted by a working capital contribution of $56.5 million, meaning underlying operating cash flow was approximately $30 million and after taking into account normalized taxes and lease payments, approximately $32 million.

Investor Relations with Trican Well

Total capital expenditures were nearly $26 million, resulting in net free cash flow of $6 million. Looking at the first half of 2024 results, we see reported operating cash flow of $49 million. Adjusted for working capital changes, a normalized tax payment and lease costs of $2.4 million, adjusted operating cash flow was $92 million. With total capital expenditures of $41.2 million, net free cash flow was approximately $51 million, or $0.25 per share at the current share count.

However, not all capital expenditures are created equal. In Trican’s case, the company spent C$11.9 million and C$15.7 million on growth capital expenditures in the second quarter and the first half of 2024, respectively. This means that the underlying sustainable free cash flow – excluding capital expenditures for growth – in the first half of the current fiscal year was about C$66.7 million, or C$0.33 per share (I used the current share count of 199.5 million shares as of the end of June, rather than the weighted average share count throughout the quarter and half year).

Over the past 18 months, the company has repurchased nearly 33 million shares of its own stock. Taking into account the exercise of stock options, the net share count decreased by approximately 30 million shares to 199.5 million. During the first half of the year, Trican repurchased shares at an average share price of approximately C$4.3.

And thanks to its very solid balance sheet, Trican can just keep buying back shares. At the end of June, the company had positive working capital of almost 150 million Canadian dollars, of which 36 million Canadian dollars were held in cash. There is no debt on the balance sheet (apart from lease liabilities and some deferred tax liabilities), meaning that with its current market capitalization of almost exactly 1 billion Canadian dollars, a current share price of around 5.05 Canadian dollars and a share count of 199.5 million, that gives it an enterprise value of 970 million Canadian dollars.

With first-half adjusted EBITDA of C$120 million and expected full-year adjusted EBITDA of C$240 million (vs. C$235 million EBITDA in fiscal 2023), the Company currently trades at an EV/EBITDA multiple of 4. This is very reasonable for a company with a “through-the-cycle” exposure (as it provides services across the drilling, completion and production cycle).

Investment thesis

Trican Well Service expects the next few years to be good for its business. The company expects the commissioning of LNG Canada (a new LNG facility on the West Coast) to boost demand for fracking, cementing and coiled tubing as demand increases thanks to the new facility and will boost natural gas production. Trican expects the second half of 2024 to remain “robust,” but not as busy as the second half of 2023. That’s not really a surprise considering the Canadian natural gas sector has struggled with spot prices of C$1/mcf or less for an extended period this summer.

Although the result in the second half of the year is unlikely to be surprisingly good, it is important to understand that about 2/3rd of the full-year maintenance capital expenditures were already spent in the first half of the year. Even if there is no significant growth at the EBITDA level, net free cash flow should increase in the second half compared to the first half. I also have little doubt that the company will renew its share buyback plan. It has clearly stated that it will continue to buy back shares and will only consider mergers and acquisitions if the returns from mergers and acquisitions are higher than the impact of a share buyback plan.

I do not currently hold a position in Trican Well Service, but the current volatility in the financial markets and the oil markets could potentially create an interesting opportunity to acquire the stock.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these securities.