")

AntonioSolano

introduction

The average US consumer is the most important question the market is trying to answer right now. Most people expect the consumer to reduce spending. However, there is uncertainty about the extent, areas and impact of this reduction. It is not yet known whether this will have a significant impact on customer-centric businesses.

Companies like Costco (COST), Walmart (WMT), and Amazon (AMZN) are still trading at or near their all-time highs. This means that the market is not expecting a decline for these companies, at least in the short term.

I have published a comprehensive analysis of the US consumer on The Alpha Oracle website and several articles based on that research on Seeking Alpha. What is clear from my findings is that consumers are increasingly switching to cheaper products in various forms. While this trend has had a negative impact on companies like McDonald’s, some will benefit. It.

Shopify (NYSE:SHOP) is one of them. The business benefits from many factors, and the trend toward cheaper prices is just one of them. The company continues to report strong earnings growth, driven by both dealer growth and shopper activity.

The stock appears cheap based on current and historical multiples. In addition, I believe the company is transforming from a growth company to a more established and mature company. With its strong balance sheet, it could soon start rewarding its investors in a variety of ways.

Therefore, Shopify deserves a “Buy” rating.

Business description

Shopify defines itself as a leading global commerce company that provides the necessary infrastructure and tools to start and grow a global commerce business. I believe that is an accurate summary of its business model.

The company enables merchants around the world to create their brands, leverage multiple channels and manage international traffic. It provides access to a multi-channel frontend while merchants benefit from a single, integrated backend.

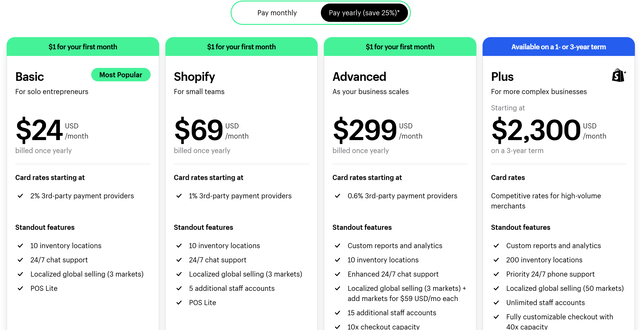

Shopify offers tiered plans that merchants can subscribe to based on their size and the tools they need to build their business. These plans allow merchants to accept payments, secure working capital, have Shopify handle shipping and order fulfillment, give their customers the ability to use buy now, pay later options, and launch marketing campaigns.

That’s why Shopify invests in the success of its merchants. A successful and growing merchant sells more, eventually moves to a premium payment plan, and uses more of Shopify’s tools. Supporting its merchants is an essential part of Shopify’s organic growth strategy.

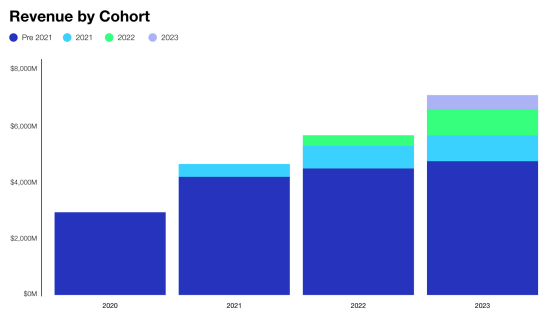

The chart below illustrates the above points. As merchants grow, they increase their spending on Shopify. This is a long-term trend that benefits Shopify.

Shopify Annual Report

Additionally, Shopify generates high recurring revenue from its merchant services and its fixed payment plans. Currently, the cheapest plan starts at $24 per month with an annual commitment.

shopify.com

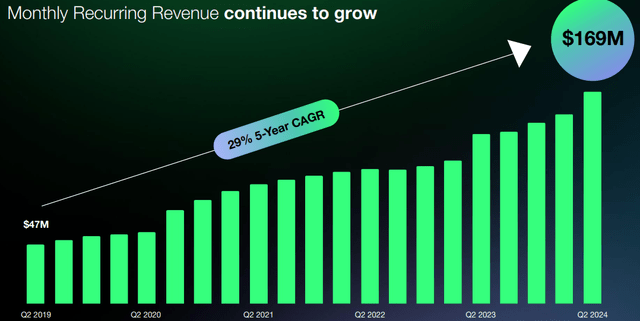

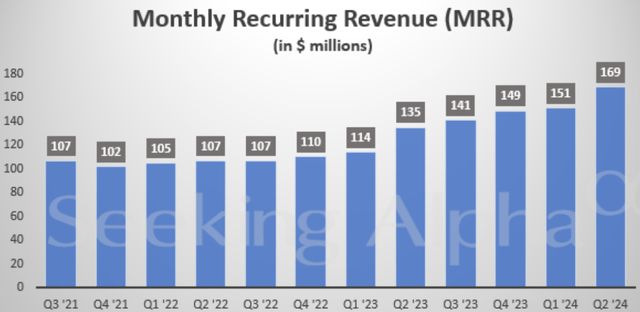

Thanks to these fixed payment plans and the company’s support of merchant growth, Shopify has been able to consistently increase its revenue, with monthly recurring revenue increasing nearly every quarter since the second quarter of 2019.

Shopify Q2 2024 Deck

As of December 2023, Shopify worked with millions of merchants from 175 countries. More than half of these merchants are located in North America, 27% in EMEA, 14% in APAC, and the remaining 5% in Latin America. US merchants generated 66% of total revenue in fiscal year 2023. This company had a 10% share of the US e-commerce market.

Strong earnings change market expectations

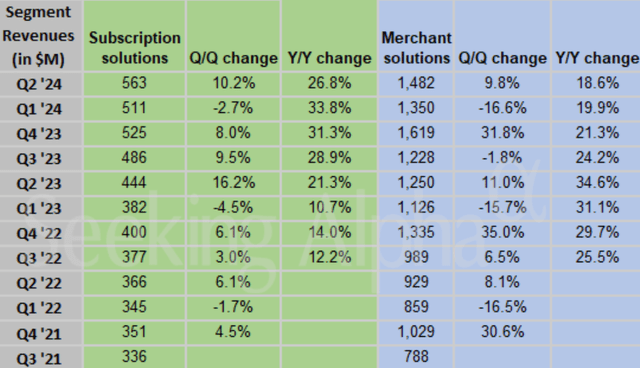

Despite concerns about consumer weakness, Shopify reported strong second-quarter results. Revenue grew 21% year-over-year and beat estimates. The company also beat EPS estimates and gross merchandise volume (“GMV”) grew 22% year-over-year.

Subscription solutions, the recurring revenue part of the business, saw revenue increase 27%, driven by the growing number of merchants and price increases on subscriptions, underscoring the pricing power the company has over merchants. Merchants face significant switching costs and few competitors offer Shopify’s services.

I’m looking for Alpha I’m looking for Alpha

The stock has risen 38% since the earnings release, reflecting improved expectations.

Unaffected by weak consumption

The company seems to be navigating the current weak consumer environment quite well. This may sound counterintuitive at first, but it could actually benefit from this consumer weakness.

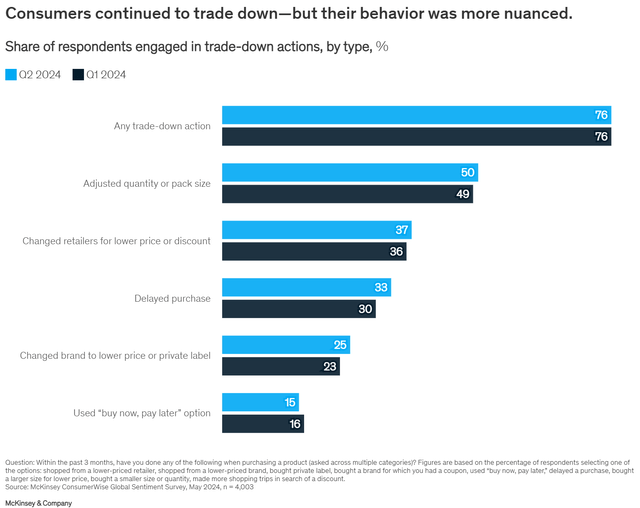

According to a McKinsey study, consumers respond to declining purchasing power by buying cheaper products. In this study, 76% of respondents said they buy cheaper products, 37% switch retailers to get lower prices or discounts, and 25% switch brands to get cheaper prices.

McKinsey

Despite this trend, Shopify’s business remains strong, suggesting that as these consumers move to lower-priced products, they may turn to Shopify merchants. CFO Jeff Hoffmeister mentioned that the company continues to gain market share in the U.S. e-commerce market and abroad. This statement is another indicator of the strong demand the company is experiencing.

A pioneer for global entrepreneurship

In addition to its continued strength, Shopify is also strengthening its brand image as a supporter for entrepreneurs looking to start a commerce business.

The ease of starting a trading business, regardless of size, encourages potential merchants to sign up with Shopify and try their luck in global commerce. The tools provided by Shopify allow investors to focus on their products while Shopify takes care of the rest.

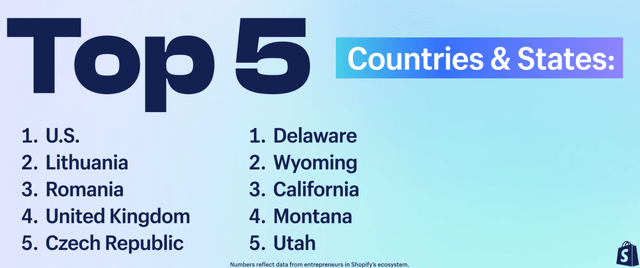

The company has actually launched the Shopify Entrepreneurship Index, which tracks global entrepreneurship in 40 countries, including the US. According to the index, Shopify entrepreneurs’ contribution to GDP, employment, and exports has been steadily increasing. The US ranks first in the economic influence of entrepreneurs and also has the highest number of entrepreneurs in the Shopify ecosystem.

shopify.com

Evaluation

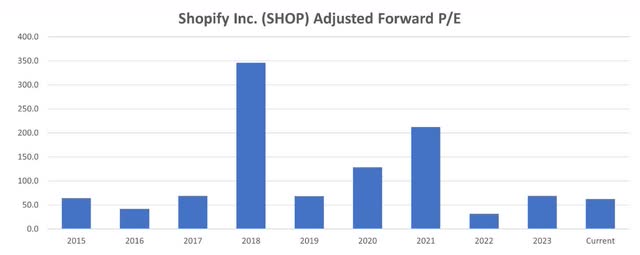

Using a DCF model as a valuation method for Shopify is challenging, as it is for many other high-growth companies. Even with a perfectly set-up model, it remains difficult to estimate long-term growth and determine an appropriate discount rate. From personal experience, I believe DCF works better for more established companies, so I will value Shopify using its adjusted forward price-to-earnings ratio (“Fwd. P/E”).

2018 and 2021 appear to be outlier years due to weak results in 2019 and 2022. Excluding them and including 2022, when the stock fell about 65%, gives an average P/E of 71.7. The stock is currently trading below this historical average.

S&P Capital IQ

With strong tailwinds such as significant growth in the number of merchants, pricing adjustments, and the fact that consumers appear to be switching to Shopify’s merchants, I believe the growth opportunity is higher than ever, and therefore the stock should trade at a higher multiple than the historical average.

Based on this observation, I conclude that the stock is undervalued.

In addition, I believe it is quite possible that the company will begin to reward its shareholders in alternative ways.

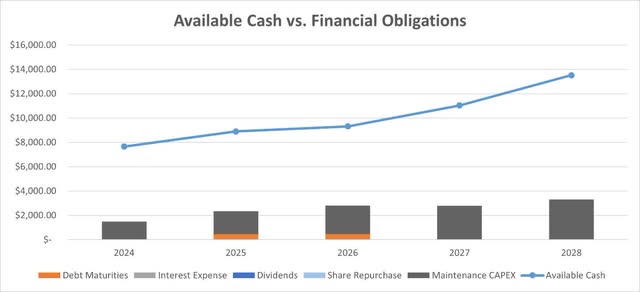

Using my cash flow projections, I calculate the company’s cash balance at the end of each year, as well as its financial obligations. The chart below shows that Shopify has more than enough cash to cover its maintenance capital expenditures, maturing debts, and potential growth investments.

S&P Capital IQ & Author

Even after covering these obligations, the company will have a significant surplus of cash. This can be distributed to shareholders in the form of dividends or share buybacks. This would drive up the share price.

Diploma

I sought to understand the average U.S. consumer, their behavior, and the impact of that behavior on various industries and companies. While retail may seem like the sector most vulnerable to consumer weakness, a closer analysis reveals more complex dynamics.

Consumers don’t suddenly stop spending money. They find ways to save. A key part of that saving is finding alternatives. I believe Shopify’s strong earnings suggest that consumers may be switching to Shopify merchants.

The business remains strong despite weakening consumers, with increasing gross merchandise volume, recurring revenue and increasing dealer base. In addition, price adjustments underscore the company’s pricing power and the benefits it is achieving through switching costs.

Because the stock appears undervalued and there is significant excess cash that could be returned to shareholders, Shopify deserves a Buy rating.