seems to be using debt quite sensibly")

Howard Marks put it nicely when he said, “The possibility of permanent loss is the risk that worries me… and that worries every practical investor I know.” So it seems that the smart money knows that debt – which usually accompanies bankruptcies – is a very important factor when assessing the risk of a company. The important thing is, Allegion plc (NYSE:ALLE) is in debt. But is this debt a cause for concern for shareholders?

When is debt dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it back, either by raising capital or with its own cash flow. If the company can’t meet its legal obligations to pay off debt, shareholders could end up empty-handed. However, a more common (but still painful) scenario is that the company has to raise new equity at a low price, resulting in permanent dilution for shareholders. By replacing dilution, however, debt can be an extremely good tool for companies that need capital to invest in high-return growth. When considering how much debt a company has, you should first look at its cash and debt together.

Check out our latest analysis for Allegion

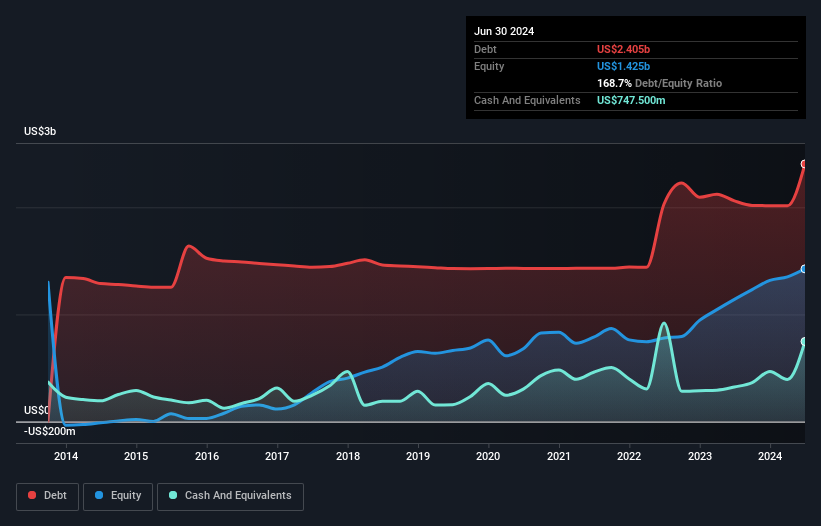

How much debt does Allegion have?

As you can see below, Allegion had $2.40 billion in debt at the end of June 2024, up from $2.06 billion a year ago. Click on the image for more details. However, that compares to $747.5 million in cash, resulting in net debt of about $1.66 billion.

How strong is Allegion’s balance sheet?

According to the last reported balance sheet, Allegion had liabilities of $1.03 billion due within 12 months and liabilities of $2.32 billion due beyond 12 months. These liabilities were offset by cash of $747.5 million and receivables of $474.1 million due within 12 months. So the company’s liabilities are $2.13 billion more than the combination of cash and short-term receivables.

With Allegion’s publicly traded shares valued at an impressive $11.7 billion in total, these liabilities are unlikely to pose a major threat, but we think it’s worth keeping an eye on the company’s balance sheet strength, as it may change over time.

We use two main ratios to inform us about the level of debt relative to earnings. The first is net debt divided by earnings before interest, taxes, depreciation, and amortization (EBITDA), while the second tells us how much earnings before interest and taxes (EBIT) covers interest expenses (or, in short, interest coverage). The advantage of this approach is that we take into account both the absolute level of debt (with the ratio of net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest coverage ratio).

Allegion’s net debt of 1.9 times EBITDA suggests it handles debt decently. And the fact that trailing-twelve-month EBIT was 9.5 times interest expense is consistent with that theme. Allegion grew its EBIT by 8.2% last year. While that hardly blows us away, it is a debt positive. There’s no doubt that we learn the most about debt from the balance sheet. But it’s future earnings, more than anything, that will determine Allegion’s ability to maintain a healthy balance sheet going forward. So if you’re focused on the future, you can look at free Report with analysts’ profit forecasts.

However, our final consideration is also important because a company can’t pay off debt with book profits; it needs cash. So we really need to check whether that EBIT is leading to corresponding free cash flow. Over the last three years, Allegion generated solid free cash flow, equal to 64% of its EBIT, which is about what we’d expect. This free cash flow puts the company in a good position to pay down debt if needed.

Our view

The good news is that Allegion’s proven ability to cover its interest expense with its EBIT has us as happy as a fluffy puppy with a toddler. And that’s just the beginning of the good news, because its EBIT to free cash flow conversion is also very encouraging. Looking at all of the above factors together, we notice that Allegion can handle its debt pretty comfortably. Of course, this debt can increase return on equity, but it also brings more risk, so it’s worth keeping an eye on. There’s no doubt that we learn the most about debt from the balance sheet. But ultimately, every company can contain risks that exist off the balance sheet. For example, we found that 1 warning sign for Allegion that you should know before investing here.

If, after all that, you’re more interested in a fast-growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage all your stock portfolios in one place

We have the the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of portfolios and see your total amount in one currency

• Be notified of new warning signals or risks by email or mobile phone

• Track the fair value of your stocks

Try a demo portfolio for free

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.