")

The Good Brigade

One of my best calls in recent years was a home builder named M/I-Houses (MHO). In my last article about the company, published in early January In 2023, I acknowledged that the company was doing quite well. While I did say that the company could run into trouble in the short term, I ultimately concluded that the long-term picture for the company was positive. This led me to maintain a Buy rating on the company to reflect my view that shares would outperform the broader market for the foreseeable future.

And they have done better! Since this article was published, the stock has risen 235.4%. That dwarfs the 46.3% upside of the S&P 500 over the same period. But if we look at when I originally rated the stock, It If you buy back in August 2022, the picture looks even better. Shares are up 258.6%, while the S&P 500 is up just 34.4%. After such a massive uptrend, you might think I’d be willing to downgrade the stock. But given current share prices, both in absolute terms and relative to similar companies, I’d argue there’s still more upside.

A great home for your money

Author – SEC EDGAR Data

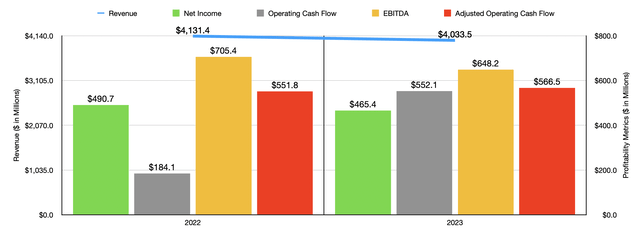

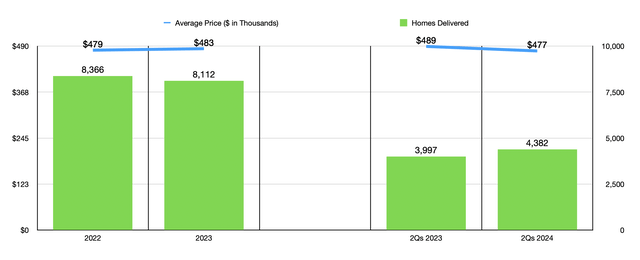

Given the time that has passed, perhaps it’s best to start with the company’s performance over the past few years. In 2022, the company’s revenue was $4.13 billion. In 2023, revenue was lower at $4.03 billion. That’s a 2.4% year-over-year decline. Although the company benefited from an increase in the average price of a home delivered from $479,000 to $483,000, it suffered from a decline in deliveries from 8,366 to 8,112 homes. That’s not too surprising. After all, the real estate market has been going through something of a soft patch due to inflationary pressures and the resulting high-interest rate environment designed to combat that inflation. Because a home is typically the largest investment an individual or family makes in their lifetime, and because it often requires long-term financing, higher prices and high interest rates make buying a home far more expensive.

Author – SEC EDGAR Data

As revenues fell, earnings and cash flows largely followed this trend. Net income fell from $490.7 million to $465.4 million. Operating cash flow did increase from $184.1 million to $552.1 million, but adjusting for changes in working capital showed a more modest increase from $551.8 million to $566.5 million. Then there’s EBITDA. And just like net income, it took a hit, falling from $705.4 million to $648.2 million.

Author – SEC EDGAR Data

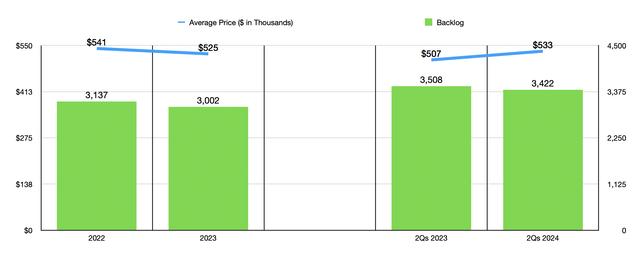

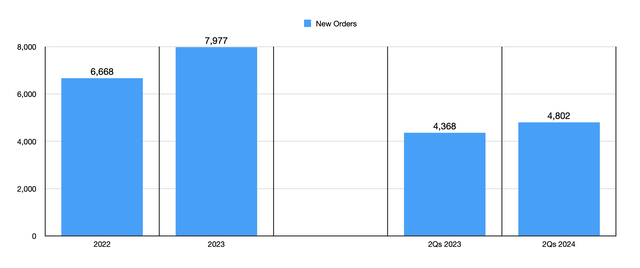

It’s worth noting that the company has benefited from a surge in new orders. Customers ordered 7,977 homes in 2023, a significant increase from the 6,668 orders placed last year. Unfortunately, this wasn’t enough to prevent the company’s backlog from falling from 3,137 homes to 3,002. While the cancellation rate dropped from 14.3% to 11.4%, it’s still higher than it should be. In addition, the backlog is less valuable per home than it was then. In 2022, the average price of a home in the backlog was $541,000. That figure had fallen to $525,000 by the end of last year.

Author – SEC EDGAR Data

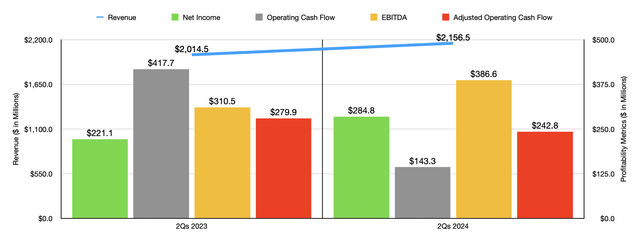

Looking ahead to fiscal 2024, we saw a small bright spot. First-half revenue was $2.16 billion. That’s an improvement from the $2.01 billion reported during the same period in 2023. The company benefited from an increase in homes delivered from 3,997 to 4,382. However, that was partially offset by a drop in the average price of a delivery from $489,000 to $477,000. While that may not seem like a lot, when applied to the number of homes delivered during that period, that’s an additional $52.6 million in revenue over the company’s top line. And since the company is already generating positive profits, every penny of that would have been a penny higher in pre-tax profit.

Author – SEC EDGAR Data

Although the average price for a home delivery fell, the increase in deliveries was enough to boost net income by 28.8%, from $221.1 million to $284.8 million. Other profitability metrics were mixed. For example, operating cash flow fell from $417.7 million to just $143.3 million. However, if we take into account the changes in working capital, the decline is more modest, from $279.9 million to $242.8 million. On the other hand, the company saw an improvement in EBITDA, with this figure increasing from $310.5 million to $386.6 million.

From the end of last year to the end of the second quarter, M/I Homes saw an improvement in its backlog. At the end of the quarter, the backlog totaled 3,422 homes. However, this is still less than the 3,508 homes the company had at the end of the second quarter of 2023. As disappointing as this is, it is offset by a year-over-year increase in the average price of a home in the backlog. This rose from $507,000 last year to $533,000 this year. The backlog would have been even worse if the cancellation rate had not improved from 12% to 9%. Frankly, I am not surprised to see the backlog grow quarter-over-quarter. This is because management signed contracts for 4,802 new homes in the first half of this year. That’s 9.9% more than the 4,368 homes signed during the same period last year.

Author – SEC EDGAR Data

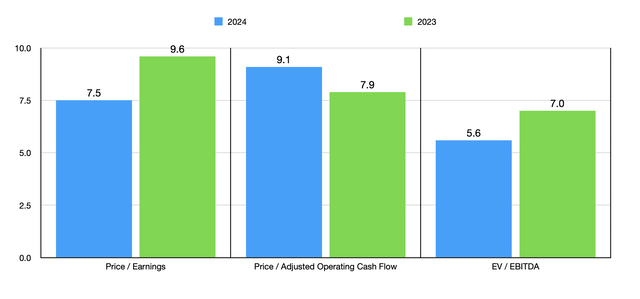

Unfortunately, we don’t really know what to expect for the rest of the year from a revenue and earnings perspective. But if we annualize the results to date, we’d be looking at income of $599.5 million, adjusted operating cash flow of $491.4 million, and EBITDA of $807.1 million. Using these estimates, as well as historical results going into 2023, I was able to value the company as shown in the chart above. Although the stock is more expensive on a forward basis when it comes to price-to-earnings to adjusted operating cash flow, it is cheaper on the other two metrics. And in fact, it’s so cheap that it looks quite enticing. And it’s not just cheap on an absolute basis. It’s cheap compared to similar companies, too. You can see exactly what I mean in the chart below. On a price-to-earnings basis, only one of the five companies I compared M/I Homes to ended up being cheaper than it is. And for the other two approaches, our candidate ended up being the cheapest of the group.

| Pursue | Price/earnings | Price/operating cash flow | EBITDA |

| M/I-Houses | 7.5 | 9.1 | 5.6 |

| Green Brick Partners (GRBK) | 10.9 | 570.2 | 8.5 |

| Dream Finders Homes (DFH) | 10.9 | 16.5 | 9.1 |

| Century Communities (CCS) | 10.3 | 74.7 | 9.4 |

| Tri Pointe Homes (TPH) | 10.4 | 26.9 | 8.2 |

| Beazer Homes USA (BZH) | 7.0 | 25.8 | 12.3 |

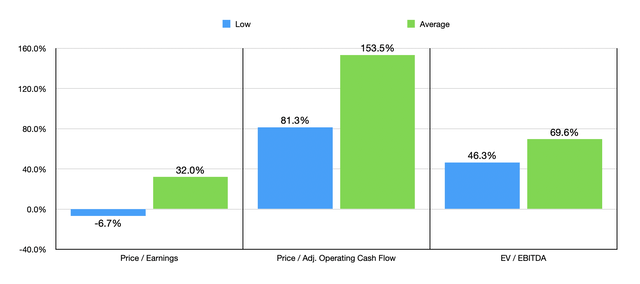

When analyzing the company, I also looked at what kind of upside potential the shares might offer, if any. In the chart below, you can see a few different scenarios. For the price-to-earnings approach, the price-to-operating cash flow approach, and the EV-EBITDA approach, I wanted to see how much upside or downside potential the shares would have if they traded at multiples of the cheapest of the five companies I compared them to. In the worst case scenario, we get a downside of 6.7%. However, the other two metrics give an upside potential of between 46.3% and 81.3%. Then I did the same with the average of those companies. In this case, for the price-to-operating cash flow approach, I excluded the two most expensive companies. This is because they are very obvious outliers. Even so, we get an upside potential of between 32% and 153.5%.

Author – SEC EDGAR Data

Management is well aware of how cheap stocks are. On May 13 of this year, it announced a new $250 million share repurchase program, replacing the previous program that only had $103 million in capacity. After making $50.3 million in purchases in the second quarter alone, the company has $207.1 million in capacity left under that program. Year-to-date, management has repurchased $75.6 million in stock. This is in addition to the $65.3 million repurchased last year. It helps that net debt was only $79.7 million at the end of last quarter.

Take away

Fundamentally, M/I Homes is looking a bit mixed right now. But overall, I would view the picture as positive. As with other players in the space, M/I Homes will experience volatility from time to time. For example, if the U.S. economy experiences a hard landing, there could be months or even a year of underperformance. But for those who think long-term, shares look cheap enough to justify a bullish outlook. Ultimately, this consideration has led me to rate the company a Buy for now.