")

Subscribe

Perhaps one of the most difficult tasks in a cyclical industry is to trade against the economic cycle. ARC Resources Ltd. (OTCPK:AETUF) is doing just that by bringing the Attachie project online (as mentioned in the last article)) during a period of weak natural gas prices (NG1:COM). ARC is further bucking the industry by intending to make money from this project under the same hostile industry conditions. If natural gas prices recover, this company will definitely benefit from such an event. But that will be in addition to the money it is making now. Unlike many others in the industry, this natural gas producer is currently making a decent amount of money.

Production shutdowns

Until prices recover, dry gas production will be partially halted.

“After the end of the quarter, in response to record low natural gas prices in Western Canada, ARC has decided to curtail natural gas production at its sole dry gas facility, Sunrise, by approximately 250 million cubic feet per day. ARC will resume full production when natural gas prices have recovered to levels that meet ARC’s return on investment requirements.”

“On a per-well basis, the modified well design at Upper Montney is expected to result in a 40 percent increase in natural gas production in the first twelve months, with well costs increasing by only 25 percent due to more intensive completions.

As a result, Sunrise’s annual capital costs for the Upper and Lower Montney development are expected to decrease by 10 percent compared to the previous development plan.”

This quote from the second quarter earnings press release continues an industry-wide trend of withholding higher-cost dry gas production from the market while natural gas prices remain weak.

Meanwhile, the cost per MCF is declining. It is worth remembering that costs are lowest when the source starts producing, but some costs increase as production declines over time. So what started as low-cost production could become more expensive or even outright expensive a few years later.

Often, just reaching the heating season in the fall is enough for many of these wells to resume production and contribute to profit margins.

However, this company, unlike many others in the current environment, has numerous profitable options, so if production has to be halted indefinitely, there are plenty of other ways to provide the company with sufficient cash flow.

As for bad news, many companies have much worse to report.

revenue

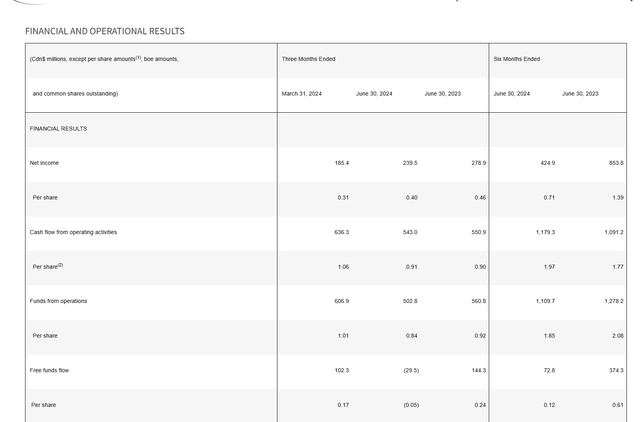

The big difference for this natural gas producer (a Canadian producer reporting earnings in Canadian dollars unless otherwise noted) is that this company makes a decent profit in this environment due to its condensate production, which is produced together with the natural gas.

ARC Resources Second Quarter 2024 Results Financial Summary (ARC Resources Second Quarter 2024 Results Press Release)

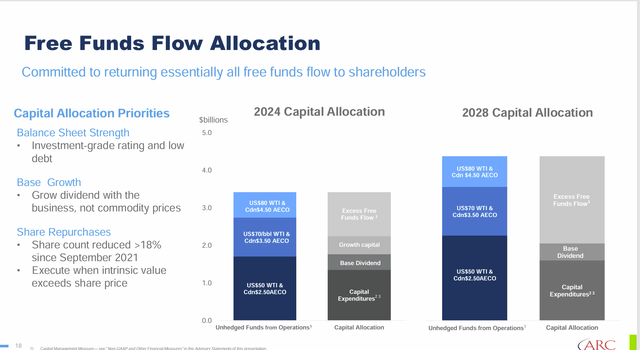

Even at the bottom of the natural gas market, this company is investing in growth projects and paying a dividend while maintaining its excellent financial strength. Companies that tend to produce above-average results over the long term are companies that do exactly what this company does.

The cost of capital tends to be lower when much of the industry is waiting for a recovery, so this company can often select low-cost services that produce another low-cost (and long-lived) asset. Such execution is as good as a competitive advantage.

Dividends

The asset reinvestment rate is low enough so that the company can pay a dividend, buy back shares and continue to invest in growth projects.

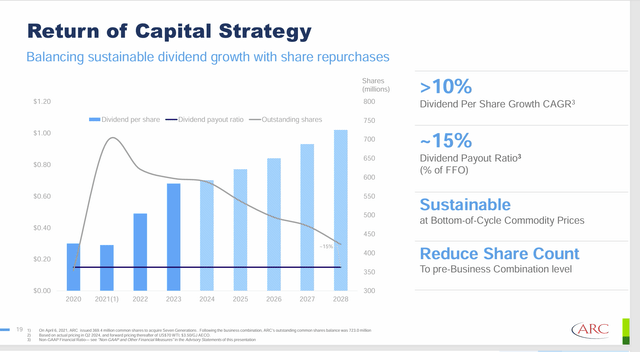

ARC Resources Launches Shareholder Return Program While Increasing Production (ARC Resources Q2 2024 Earnings Call Slides)

The Attachie project is scheduled to go into production next fiscal year, so capital expenditures for this project are almost complete. When the project is fully operational, production should increase by about 10% on top of what the company can produce now.

The dividend of C$0.17 per share is already well covered, as shown above, since the share buyback program would be the first to be scaled back if industry conditions were to deteriorate.

Furthermore, this is an investment grade idea, so the credit market is almost always open to more debt should management decide to take on more debt rather than cut growth projects or the dividend.

Idea of capital repayment

The main idea of this management is essentially to buy back the capital that was used to acquire Seven Generations (which was an all-stock deal). Therefore, at least initially, management intends to bring the number of shares outstanding to a number that existed before the merger. This is different from many buyback programs.

ARC Resources Share Repurchase Progress (ARC Resources Q2 2024 Earnings Call Slides)

According to management, outstanding shares are almost back to pre-merger levels. However, outstanding shares benefit from the additional production that Seven Generations has added to the company.

Production included a large amount of condensate, allowing the company to significantly outperform the industry average during times of weak natural gas production.

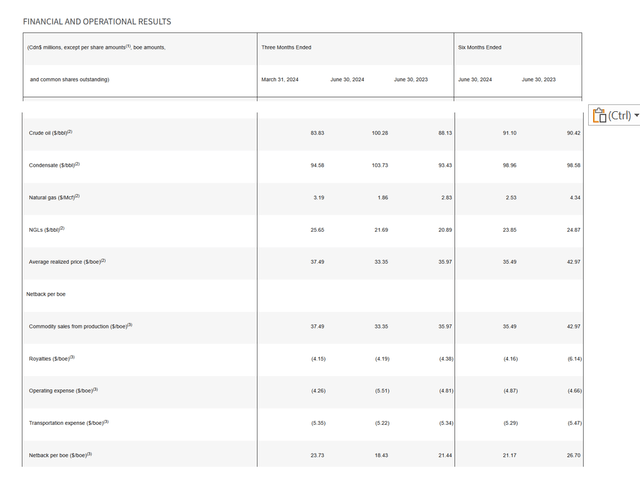

Realized prices and netback

Before merging with Seven Generations, this company was primarily a dry gas producer with some liquids-rich production. Seven Generations added a lot of condensate (and oil) to the production mix.

ARC Resources Realized Prices and Netback (ARC Resources Second Quarter 2024 Results Press Release)

What has significantly mitigated the impact of significantly lower natural gas prices compared to last year is the strength of condensate and oil prices. While some key metrics are lower than a year ago, the results compare very positively to much of the natural gas industry, which is cutting production and idling plants while hoping for higher natural gas prices.

At this company, activity remains largely at normal levels, although production is now at the lower end of guidance. The idled production can be restarted quickly. Combined with the start of production at Attachie next fiscal year, this company should be able to show some stunning production growth comparisons for such a large company.

Summary

ARC Resources has seen a profit decline that has been far better than much of the natural gas industry. The combination of very low production costs and the amount of oil and condensate produced has made it quite easy for the company to weather this period of low natural gas prices.

Perhaps most importantly, the company is still profitable and is generating a decent (if low) return on capital at what is widely considered to be a low point in natural gas prices.

The diversification brought about by the acquisition of Seven Generations has clearly had a positive impact.

This company remains a good buy due to its continued industry-wide outperformance. It’s difficult to overpay for an investment idea during an industry downturn, as the stock is sure to trade much higher when natural gas prices recover. The investment-grade rating and dividend are basically the “icing on the cake” compared to the appreciation possible when natural gas prices recover.

Risks

Every upstream company is exposed to the volatility and low predictability of future commodity prices. Any severe and prolonged downturn could significantly alter the company’s prospects.

This risk is mitigated by the fact that the company produces oil and condensate in large enough quantities to be immune to the volatility of natural gas prices. For the company to perform poorly, all of its products would have to experience a downturn at the same time. The risk of this is far lower than for a single commodity product to experience a cyclical downturn.

Price risk is also mitigated by the fact that the company has exceptionally low production costs. The biggest risk is that the company will run out of low-cost locations at some point in the future. However, that would mean that the technological advances that regularly sweep the industry would come to a halt. This is also an unlikely scenario.

While there are always risks involved in investing in a company operating in the fast-moving natural resources industry, ARC Resources Ltd. is in one of the better positions to do so. Its investment-grade rating reflects this.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these securities.