shares could be in for some unpleasant surprises")

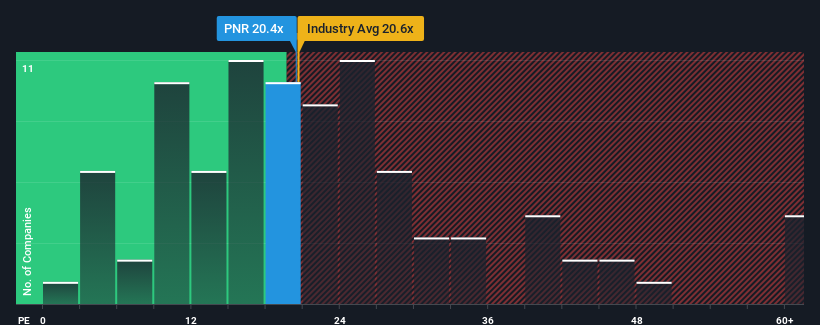

When nearly half of the companies in the United States have a price-to-earnings (P/E) ratio of less than 17x, you may consider Pentair plc (NYSE:PNR) as a stock that may be worth avoiding with its P/E ratio of 20.4. However, the P/E ratio might be high for a reason and further research is needed to determine if it is justified.

Pentair has certainly done well recently, as its earnings growth has been positive while most other companies’ earnings have been declining. The P/E ratio is probably high because investors believe the company will continue to weather the general market headwinds better than most. You’d better hope so, otherwise you’re paying a pretty high price for no particular reason.

Check out our latest analysis for Pentair

Would you like to know how analysts assess Pentair’s future compared to the industry? In this case free Report is a good starting point.

How is Pentair growing?

To justify its P/E ratio, Pentair would need to deliver impressive, above-market growth.

Looking back, last year saw the company achieve an exceptional 33% increase in earnings. In addition, over the last three years, EPS has seen an excellent overall increase of 40%, helped by short-term performance. Accordingly, shareholders would likely have welcomed these medium-term earnings growth rates.

According to analysts, earnings per share are expected to grow at 11% per year over the next three years. With the market expected to deliver 11% growth per year, the company is positioned for a comparable result.

With that in mind, we find it interesting that Pentair is trading at a high P/E relative to the market. It seems that most investors are ignoring the rather average growth expectations and are willing to pay more to own the stock. However, additional gains will be hard to come by as that earnings growth will likely weigh on the share price eventually.

The most important things to take away

Although the price-earnings ratio should not be the deciding factor in whether or not you buy a stock, it is still a useful indicator of earnings expectations.

We have noted that Pentair is currently trading at a higher than expected P/E ratio as its forecast growth is only in line with the overall market. At the moment, we are unhappy with the relatively high share price as its forecast future earnings are unlikely to sustain such positive sentiment for long. This puts shareholders’ investments at risk and potential investors risk paying an unnecessary premium.

We don’t want to spoil the fun too much, but we also found 1 warning sign for Pentair that you need to consider.

If you are uncertain about the strength of Pentair’s businesswhy not explore our interactive stock list with solid business fundamentals for some other companies you may have missed.

New: Manage all your stock portfolios in one place

We have that the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of portfolios and see your total amount in one currency

• Be notified of new warning signals or risks by email or mobile phone

• Track the fair value of your stocks

Try a demo portfolio for free

Do you have feedback on this article? Are you concerned about the content? Get in touch directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.