People are waiting for interest rates and prices to fall while supply continues to rise.

By Wolf Richter for WOLF STREET.

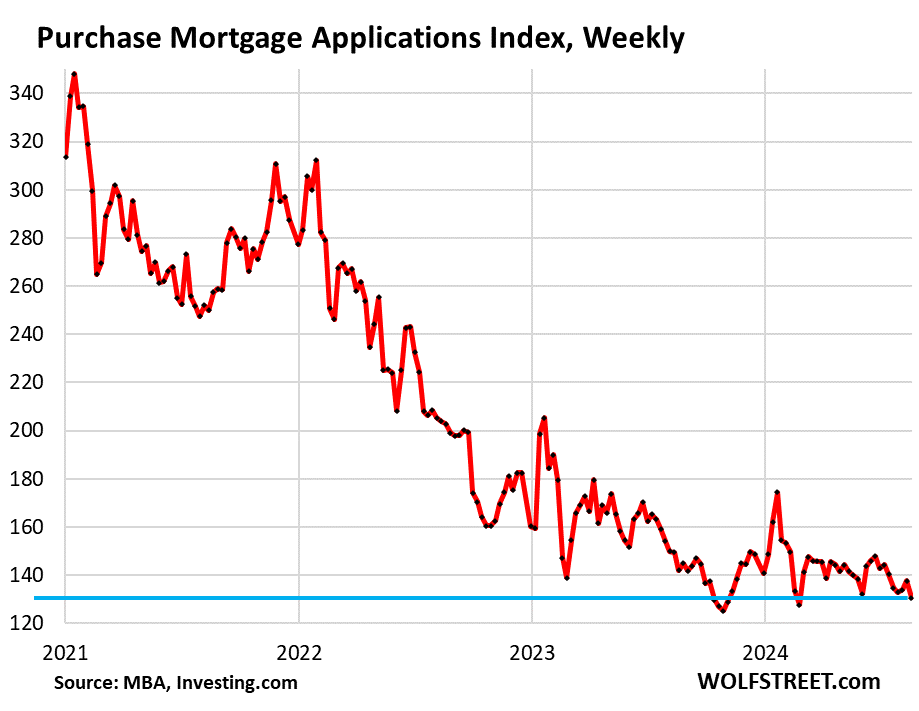

According to the Mortgage Bankers Association, mortgage rates have dropped to 6.50% today, the lowest since May 2023. But instead of reigniting demand for homes from buyers in need of mortgages, these falling rates have caused potential buyers to wait for further falling mortgage rates and falling home prices because prices are way too high, further reducing demand and driving applications for mortgages to purchase a home to historic lows.

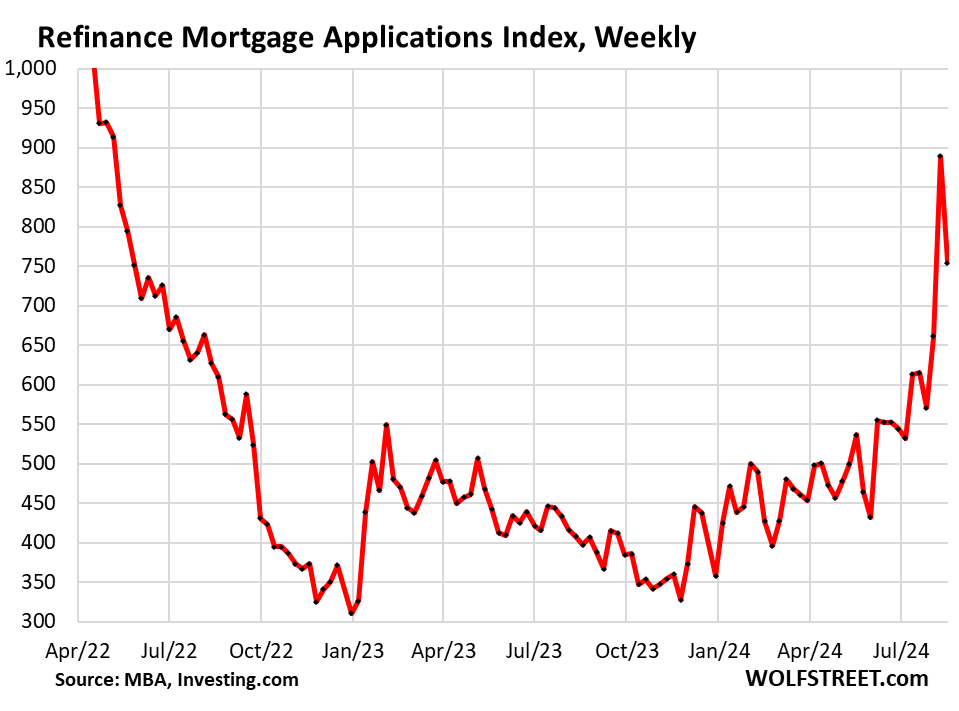

However, lower mortgage rates have revived applications to refinance existing mortgages, and the number of mortgage refinance applications has jumped in recent weeks, doubling from the historic low seen last fall. This increase in refinance applications is not affecting the housing market, but it is accelerating the pace of the Fed’s QT because it is causing mortgage-backed securities (MBS) to disappear from the Fed’s balance sheet more quickly, and we are seeing the early signs of this.

The average conforming 30-year fixed-rate mortgage rate fell another 4 basis points to 6.50% in the latest reporting week, the lowest level since May 2023, the Mortgage Bankers Association said today. This indicator of mortgage rates has been above 6% since September 2022.

People are on a buyer’s strike, waiting for lower interest rates and prices.

Home prices are too high even for cash buyers and institutional investors; purchases of existing homes have fallen sharply amid rising supply; and the number of mortgage applications to buy a home has fallen by almost half from pre-pandemic levels in 2019 and fell even further in the most recent reporting week.

The purchase mortgage application index is now only slightly above its November 2023 level, when it fell to its lowest level since 1995 following a rise in mortgage rates to 7.8%.

Mortgage applications are an early indicator of home demand and sales volume:

The increase in mortgage refinancing applications will accelerate the Fed’s QT.

But since the beginning of 2024, mortgage applications to refinance a home have been zigzagging upward from very low levels. And in early July, when mortgage rates fell, refinance applications began to skyrocket.

Last week, the index reached its highest level of activity since April 2022, the start of the rate hike cycle. In the current week, mortgage applications declined from that increase, but were still the highest since May 2022. Since last fall, refinance applications have more than doubled. Rising mortgage refinances are accelerating the pace of the Fed’s QT.

In terms of the Fed’s QT, mortgage-backed securities (MBS) are removed from the Fed’s balance sheet when the underlying mortgages are paid off through regular mortgage payments or when the mortgaged home is sold or the mortgage is refinanced. These principal payments are passed on to the MBS holders, such as the Fed.

The Fed’s monthly MBS outflow had been slow to begin with, as mortgage rates had already soared before the Fed began QT, home purchase volumes had collapsed, and refinancing volumes had collapsed. By early 2024, the pace of MBS outflows was about $14 billion per month due to the historic collapse in mortgage repayments.

But these August refinancings are the highest since the Fed began QT in the summer of 2022. The QT pace for MBS is approaching $20 billion per month, reflecting higher refinancing volumes this spring. The surge in refinancing applications since early July will accelerate the pace of the Fed’s QT if pass-through principal payments from the paid-off old mortgages actually reach the Fed.

A future increase in home sales and associated higher mortgage repayments will further accelerate the Fed’s interest rate hikes.

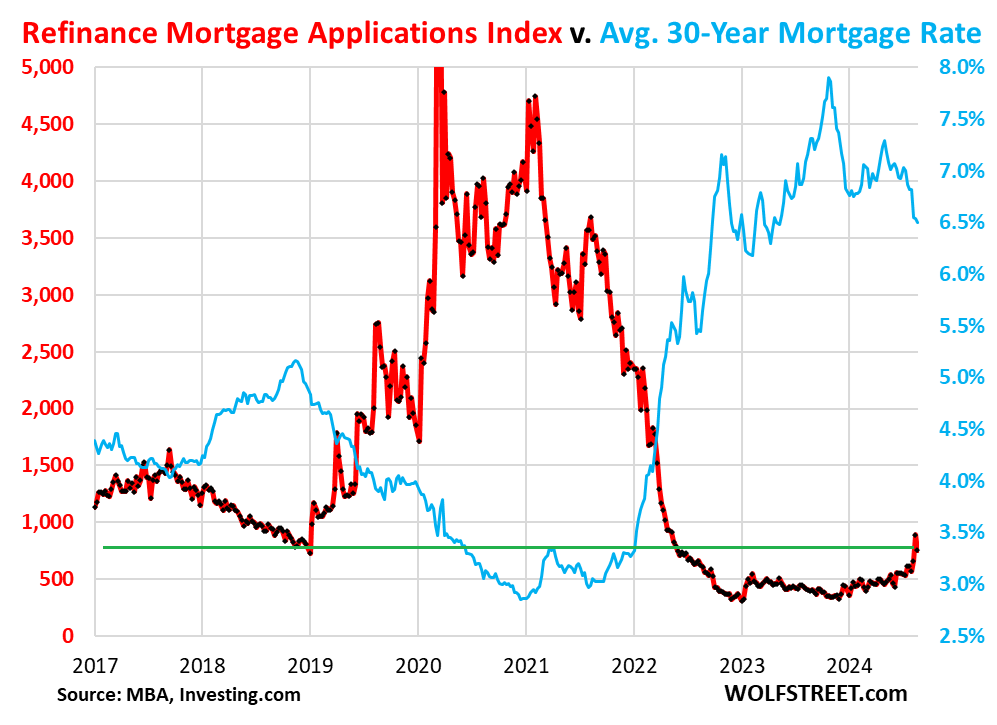

In this longer-term chart, which includes the historical increase in refinance applications during the 3% mortgage era, we can see how refinance applications (red) have nearly doubled since their lows last November, while mortgage rates (blue) have fallen.

If you enjoy reading WOLF STREET and want to support it, you can donate. I really appreciate it. Click on the beer and iced tea mug to find out how:

Would you like to be notified by email when WOLF STREET publishes a new article? Sign up here.

![]()