")

Naturgy Chile Gas Natural SA (SNSE:NTGCLGAS) failed to move the stock market despite its solid earnings report. Our analysis suggests that this could be because shareholders noticed some concerning underlying factors.

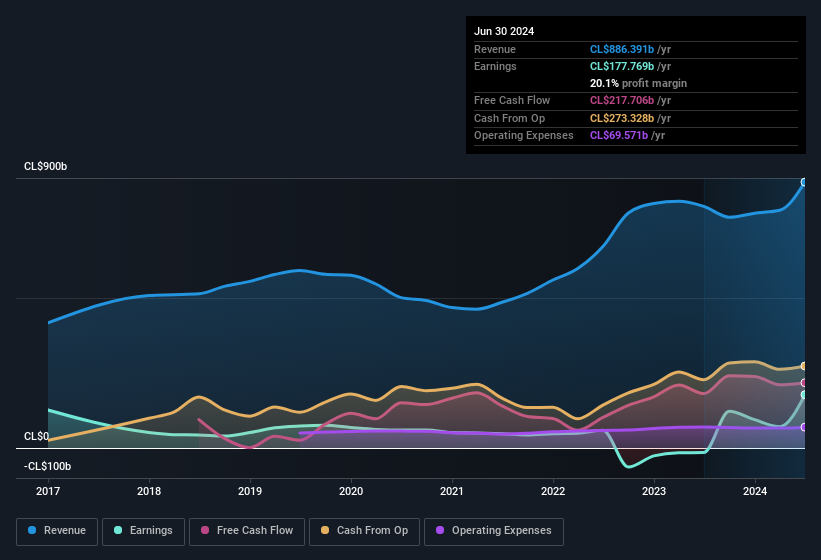

Check out our latest analysis for Naturgy Chile Gas Natural

The impact of unusual items on profit

For anyone looking to understand Naturgy Chile Gas Natural’s profit beyond the statutory numbers, it’s important to know that statutory profit over the last twelve months was driven by CL$98 billion worth of special items. While we like to see profit increases, we are a little more cautious when special items have made a big contribution. When we analyzed the numbers of thousands of listed companies, we found that an increase from special items in a given year is often not repeated next year. And that is to be expected, as these increases are described as “unusual”. Assuming these unusual items do not reappear in the current year, we would therefore expect a weaker profit next year (i.e. in the absence of business growth).

Note: We always recommend investors check balance sheet strength. Click here to access our balance sheet analysis of Naturgy Chile Gas Natural.

Our assessment of Naturgy Chile Gas Natural’s earnings performance

It could be argued that Naturgy Chile Gas Natural’s statutory profits have been distorted by unusual items boosting profits. For this reason, we believe Naturgy Chile Gas Natural’s statutory profits could be better than its underlying earnings power. The good news is that the company generated a profit over the last twelve months, despite its previous loss. Ultimately, it’s important to consider more than just the factors mentioned above if you want to properly understand the company. If you want to dive deeper into Naturgy Chile Gas Natural, you should also investigate what risks it is currently facing. Case in point: We discovered 2 warning signs for Naturgy Chile Gas Natural You should be aware.

Today we’ve focused on a single data point to better understand the nature of Naturgy Chile Gas Natural’s profit. But there’s always more to discover if you can dig deeper. Some people consider a high return on equity to be a good sign of a quality company. Although this may require a little research, you may find that free Collection of companies with high return on equity or this list of stocks with significant insider holdings may prove useful.

Valuation is complex, but we are here to simplify it.

Discover if Naturgy Chile Gas Natural could be under- or overvalued with our detailed analysis, with Fair value estimates, potential risks, dividends, insider trading and the company’s financial condition.

Access to free analyses

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.