")

Subscribe

Last Friday, Saturn Oil & Gas Inc. (TSX:SOIL:CA, OTCQX: OILSF) announced the initiation of a share buyback – the event I have been waiting for since last year. I have wrote an article about Saturn last Augustand with the puzzle pieces finally falling into place, it’s time to revisit the investment thesis and my expectations regarding future investment returns.

I started buying Saturn stock over two years ago. Since then, they have completed a transformative acquisition of Ridgeback Resources Inc., endured a period of unpleasant commodity prices and let tens of millions of shares worth of warrants expire worthless, paid off a ton of debt, made another acquisition and a corresponding debt refinancing, and finally got approval for an NCIB buyback.

In the previous article, I used both free cash flow forecasts and Reserve valuation that Saturn shares (with the usual caveats) should be worth 4-6x current price on WTI ($75-80). However, subsequent equity issuance, acquisition and refinancing change the numbers, allowing us to update the forecast of future value.

About Saturn Oil & Gas

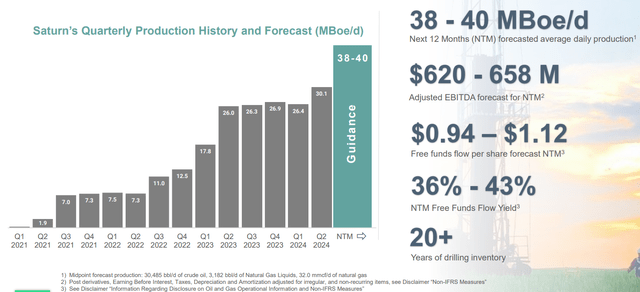

Saturn Oil & Gas Inc. is a Canadian producer of light oil, natural gas and natural gas liquids (NGLs). In the past, Saturn has grown through acquisitions. The most recent acquisition just a few months ago (in June 2024) has increased Saturn’s expected production to 38-40 MBoe/d (thousand barrels of oil equivalent per day).

Saturn Oil company presentation

Updated instructions

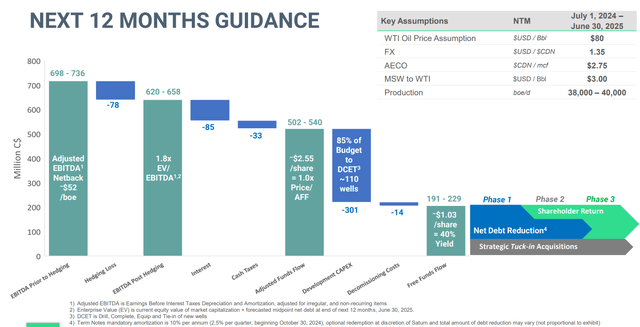

The Company provided updated guidance for 2024, the key outcome of which is targeted production of 38-40 Mboe/d and free funds flow (FFF, the same as FCF or free cash flow) of approximately CAD$200 million at a WTI value of USD$80.

Saturn Oil company presentation

While the FFF yield is now lower than when I last looked at Saturn a year ago, it is probably more realistic and includes modest growth to replace production of the asset sold in the spring, so maintenance CapEx should be lower and steady-state FFF should be higher.

The ugly loan – refinanced

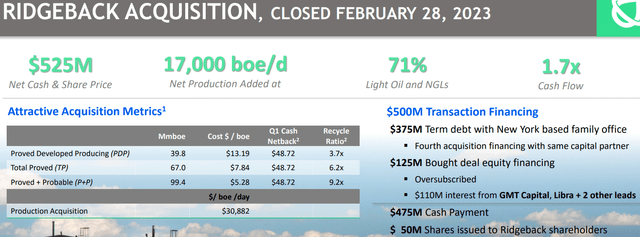

In the past, in addition to issuing stock and warrants, the company also received financing for several consecutive acquisitions from Michael Dell’s family office. Although the name was not allowed to be mentioned in press releases, it was mentioned in conference calls. The Ridgeback acquisition in 2023 was very cheap and included both the debt and equity component:

Saturn Oil company presentation

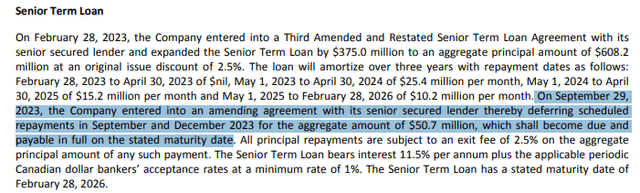

At about this time last year, Saturn’s net debt was approximately C$470 million and the company had a very aggressive repayment plan of C$25.4 million per month + 2.5% exit fee on that amount until April 2024, with lower amounts thereafter.

Saturn 23Q3 MD&A

The bad news then was this: the loan had an interest rate of about 18% and the first year amortization was very aggressive, so the company had difficulty making the principal payments and had to miss some. They even had to issue equity to fund the capital program in early 2024. The good news now is: in conjunction with the acquisition in June, the company was able to take out a loan with much better terms, reducing the interest rate to below 10% and the amortization to 10% per year for 5 years.

The cap on capital expenditure (CAD 35 million in 2025, assuming no further capital increase) has been removed. In addition, the company received a (unused) credit facility of CAD 150 million. So the company now has something it did not have in the recent past:

-

Lots of cash on the balance sheet

-

Free cash flow in excess of debt repayment (over CAD 100 million per year)

Incentives for management

While management has historically been incentivized (via the compensation structure) to grow the company, it is now more aligned with shareholders via options worth 7 million shares with a strike price of $2.50 CAD that will be granted in equal tranches when the share price reaches $4, $6 and $8 CAD. I think the incentives are now well aligned with shareholders.

And finally: shareholder returns

One of the reasons for the sharp drop in Saturn share prices was the lack of confidence in management. Year after year, the same routine was repeated, which went like this:

-

Financing an acquisition with shares (and sometimes warrants) and very expensive loans

-

Take out terrible oil hedges at low prices for several years.

-

Demonstrate an intention to drastically reduce debt and then initiate shareholder returns of an unspecified nature.

-

After a period of aggressive debt reduction, shareholders expect returns to start coming soon… Surprise! One more acquisition and the cycle repeats

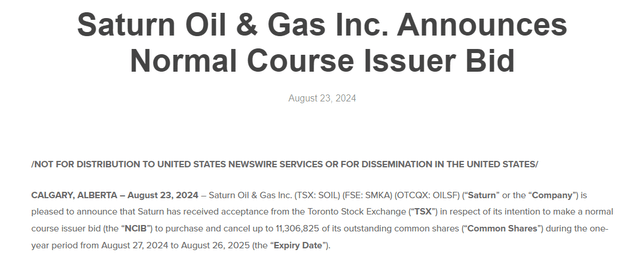

Therefore, investors were surprised on August 23, 2024 when this curious press release was issued:

Press release from Saturn Oil and Gas

I’ve been waiting for this event for a few years. I knew it was coming, but the timing was uncertain. Now the valuation gap between the share price and the intrinsic value of Saturn shares should close. And the more shares they can buy back at the current low prices, the higher the intrinsic value of the remaining shares will be.

Valuation of Saturn based on FCF

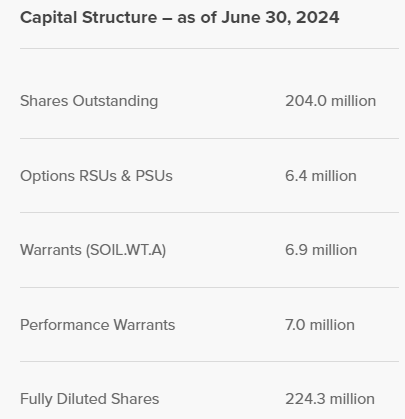

If we conservatively assume an FCF of CAD 195 million and 211 million diluted shares (excluding CAD 4 warrants or 7 million performance warrants), we arrive at an FCF of CAD 0.92 per share per year, which corresponds to an FCF yield of 35% on market capitalization (current price is CAD 2.64). With a targeted FCF yield of 12% The price target is then almost 8 CAD or 5.75 USD.or via 3-fold the current price. More if there are large buybacks.

Saturn website

Valuation of Saturn based on reserve value/NAV

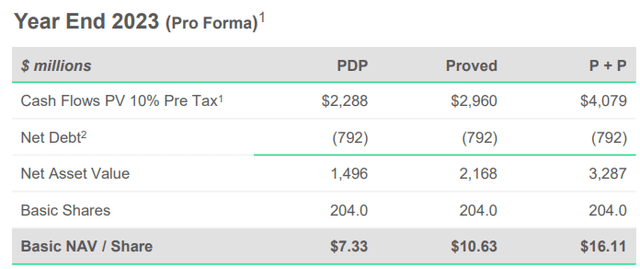

In the previous article, I had to summarize two reserve reports (from Saturn and Ridgeback). But now the company provided pro forma data:

Saturn Oil company presentation

As you can see, the shares are currently trading at only 36% of PDP (Proved Developed Produced) NAV and only 16% of 2P NAV. Conservative NAV after taxes and losses from current hedges:

1P Net Asset Value: ~8 C$ or 5.75 US$or via 3-fold the current price

2P Net Asset Value: ~11 C$ or 8 US$or via 4.2x the current price.

I do not think that a discount rate of 10% should be applied, as commodity prices will rise with inflation, but in any case we get a on reserve basis Price target of USD 8-11 (USD 5.75-8) at WTI USD 80; unbooked seats not included. This is 3 to 4.2 times the current share price.

Risks

Why does this opportunity exist? First, Saturn was a small company and grew quickly, probably unnoticed by most investors. Then there was the aforementioned lack of confidence in management. Now that many of the problems have been resolved, risks still exist.

If oil prices fall and stay low, cash generation will decline, although the company should remain profitable if it deploys capital up to ~$40 in a WTI price environment. And they can get the PDP down to about $20 WTI. But there are some risks to operational execution. Other risks include natural and other accidents, as we saw with the Alberta wildfires last year.

Diploma

Despite the risks, I like the risk-to-potential reward ratio of this investment. If the risks don’t materialize and management continues to be successful, the potential return can be significant. I like an asymmetric risk-to-reward ratio where, if I’m right, I can be a multibagger. And Saturn fits those requirements for me.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these securities.