shares could be in for some unpleasant surprises")

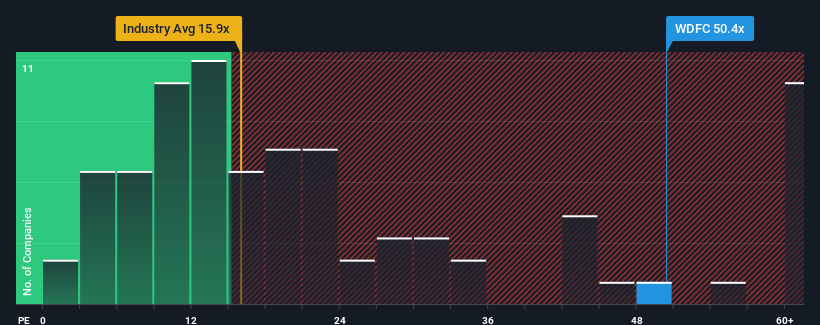

With a price-earnings ratio (P/E) of 50.4x WD-40 Company (NASDAQ:WDFC) may be sending very bearish signals right now, as nearly half of all companies in the U.S. have a P/E ratio below 18x, and even P/E ratios below 10x are not uncommon. However, it is not wise to simply take the P/E ratio at face value, as there may be an explanation for why it is so high.

WD-40 has certainly done well recently, as its earnings growth has been positive while most other companies’ earnings have been declining. It seems that many expect the company to continue to defy general market adversities, which has increased investors’ willingness to pay more for the stock. You really should hope so, because otherwise you’re paying a pretty high price for no particular reason.

Check out our latest analysis for WD-40

Would you like to know how analysts assess the future of WD-40 compared to the industry? In this case, our free Report is a good starting point.

How is WD-40 growing?

A P/E ratio as high as WD-40’s would only be truly comfortable if the company is on track to significantly outperform the market growth.

If we look at the earnings growth over the last year, the company recorded a respectable increase of 8.5%. However, this was not enough as the earnings per share recorded an unpleasant decline of 14% overall over the last three-year period. Therefore, it is fair to say that the earnings growth has been undesirable for the company lately.

Looking ahead, the two analysts who cover the company expect earnings to grow 9.1% next year, well below the 15% growth forecast for the overall market.

With that in mind, it’s alarming that WD-40’s P/E ratio is higher than most other companies. It seems that many of the company’s investors are much more optimistic than analysts indicate and aren’t willing to dump their shares at any price. There’s a good chance that these shareholders are setting themselves up for future disappointment if the P/E ratio falls to a level more in line with the growth prospects.

The last word

It is argued that the price-to-earnings ratio is not a good measure of value in certain industries, but can be a meaningful indicator of business sentiment.

We have found that WD-40 is currently trading at a significantly higher P/E than expected because its forecast growth is lower than the overall market. When we see weak earnings guidance and slower growth than the market, we suspect the share price could decline, driving the high P/E down. Unless these conditions improve significantly, it is very difficult to accept these prices as reasonable.

Many other important risk factors can be found in the company’s balance sheet. Take a look at our free Balance sheet analysis for WD-40 with six simple checks of some of these key factors.

You may find a better investment than WD-40. If you want a selection of possible candidates, check out this free List of interesting companies that trade at a low P/E ratio (but have proven that they can grow their earnings).

Valuation is complex, but we are here to simplify it.

Find out if WD-40 might be undervalued or overvalued with our detailed analysis, Fair value estimates, potential risks, dividends, insider trading and the company’s financial condition.

Access to free analyses

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.